When investing in equities, investors have two main choices: common stocks or preferred shares. Whereas the previous article in this series dealt with common shares, this article focuses on preferred shares.

The objective of the series is to provide readers with information to help create a balanced investment portfolio, with acceptable yield.

Preferred shares enjoy some form of preference over common shares: this may be with respect to payment of dividends, or preference in terms of receiving funds upon liquidation of a company, or both. Sometimes preferred shares are also convertible into common shares. Preferred shares may also be voting or non-voting. They are known as a “hybrid” instrument, because they contain certain elements of equity and certain elements of debt, usually also having higher risk then debt, but lower risk than common equity.

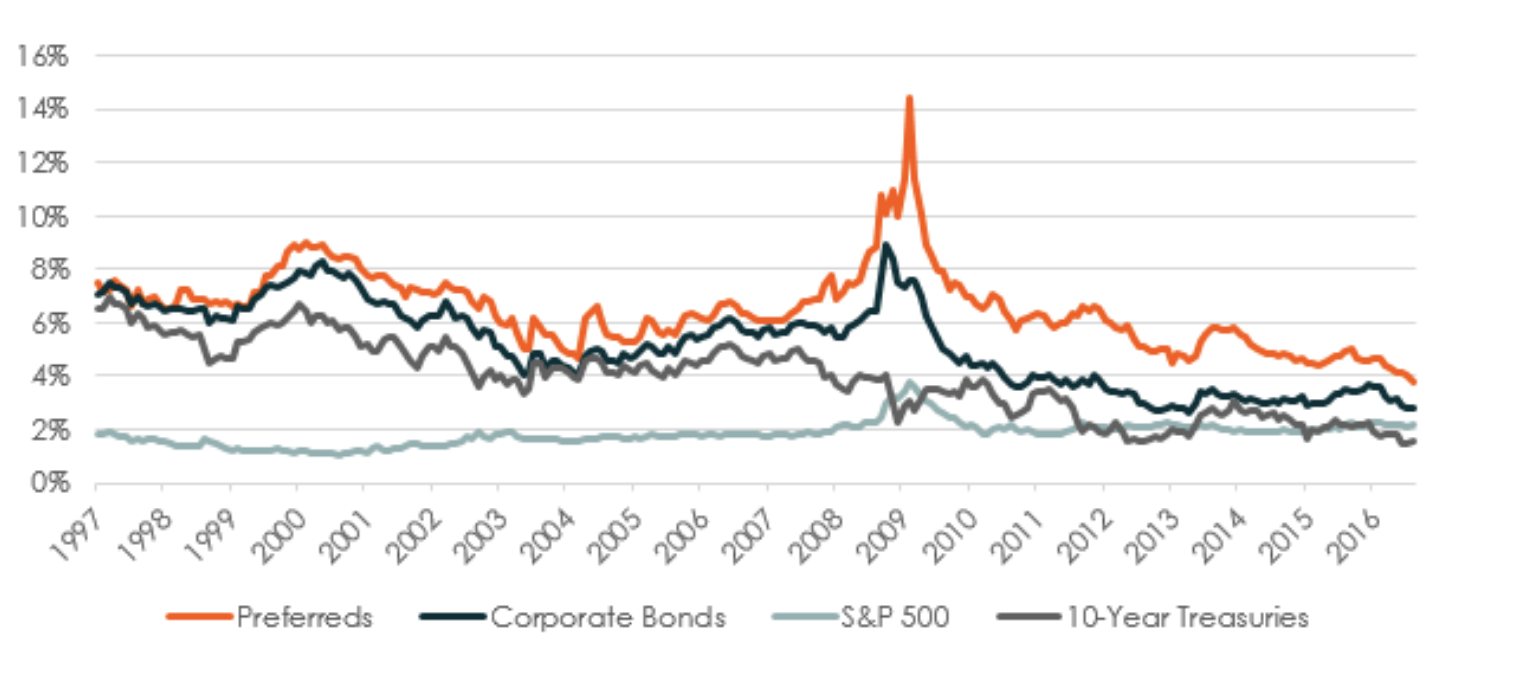

Preferred shares are a fixed-income investment i.e. it pays out fixed earnings (dividends) on a regular schedule and is issued at a “par value” for which it may be redeemed at a specified later date. Preferred shares generally have higher yield than bonds, to compensate for the higher risk, since their level of seniority is lower than bonds. Exhibit 1: Historical yield comparison over last 20 years1 An important feature of preferred shares is whether the dividends are cumulative or not. In a cumulative issue, unpaid dividends accumulate in a notional account before any dividend may be paid to common stockholders, this balance must be entirely distributed to preferred shareholders. Conversely, in a non-cumulative issue, if a dividend payment is skipped, the preferred shareholder will never receive it.

Preference shares and bonds are practical ways for a company to raise money without issuing new common shares, which are more expensive and dilute voting rights. Banks, insurance companies and utilities are typical issuers of preferred stocks. The market for preferred shares is a small one, because only a fraction of listed companies issues preference shares.

From and investors’ perspective, since preferred securities include features of both bonds and stocks, they may help diversify and strengthen a fixed-income portfolio construction. Preferreds generally show indeed relatively low correlation to other fixed income sectors and equities, which means investing in them can improve overall portfolio diversification.

In the current environment of low interest rates and rising volatility, preference shares have a certain attraction. They have typically less sensitivity to risking interest rates. In certain tax jurisdictions, preferred shares can have a significant tax advantages, particularly where dividends are taxed lower than interest.

The exhibit below is designed to give the reader an idea of several relatively well-known issuers of preferred shares, and the types of yields available.

Exhibit 2: Selected preferreds based on dividend yield2

An important feature of preferred shares is whether the dividends are cumulative or not. In a cumulative issue, unpaid dividends accumulate in a notional account before any dividend may be paid to common stockholders, this balance must be entirely distributed to preferred shareholders. Conversely, in a non-cumulative issue, if a dividend payment is skipped, the preferred shareholder will never receive it.

Preference shares and bonds are practical ways for a company to raise money without issuing new common shares, which are more expensive and dilute voting rights. Banks, insurance companies and utilities are typical issuers of preferred stocks. The market for preferred shares is a small one, because only a fraction of listed companies issues preference shares.

From and investors’ perspective, since preferred securities include features of both bonds and stocks, they may help diversify and strengthen a fixed-income portfolio construction. Preferreds generally show indeed relatively low correlation to other fixed income sectors and equities, which means investing in them can improve overall portfolio diversification.

In the current environment of low interest rates and rising volatility, preference shares have a certain attraction. They have typically less sensitivity to risking interest rates. In certain tax jurisdictions, preferred shares can have a significant tax advantages, particularly where dividends are taxed lower than interest.

The exhibit below is designed to give the reader an idea of several relatively well-known issuers of preferred shares, and the types of yields available.

Exhibit 2: Selected preferreds based on dividend yield2

For those investors who do not have enough resources to manage risk by investing in a diversified portfolio of preferred shares, there are certain Exchange Traded Funds (ETF’s) and Closed End Funds (CEF’s) that focus on preferred shares. In this context, “closed” means that once the capital is raised for the fund, it is closed to new investment. CEFs start with a set number of shares for the life of the fund and, based on market demand, they may trade well above or below net asset value. Please see the exhibit below:

Exhibit 3: Four preferred stock ETFs based on 2017 YTD performance3

In summary, preferred shares provide yet another option for investors to assemble a diversified portfolio with decent returns, even in a relatively low interest rate environment. Investors forsake the safety of bonds and the uncapped upside of common stocks. Through convertibility, the upside may nevertheless be realized.

This article is for informational purposes only, not to be construed as investment advice. Mention of specific equities if not an endorsement, merely to illustrate certain principles. It is very important to do your own investigation and analysis before making any investments based on your own personal circumstances.

Preferred shares enjoy some form of preference over common shares: this may be with respect to payment of dividends, or preference in terms of receiving funds upon liquidation of a company, or both. Sometimes preferred shares are also convertible into common shares. Preferred shares may also be voting or non-voting. They are known as a “hybrid” instrument, because they contain certain elements of equity and certain elements of debt, usually also having higher risk then debt, but lower risk than common equity.

Preferred shares are a fixed-income investment i.e. it pays out fixed earnings (dividends) on a regular schedule and is issued at a “par value” for which it may be redeemed at a specified later date. Preferred shares generally have higher yield than bonds, to compensate for the higher risk, since their level of seniority is lower than bonds. Exhibit 1: Historical yield comparison over last 20 years1

An important feature of preferred shares is whether the dividends are cumulative or not. In a cumulative issue, unpaid dividends accumulate in a notional account before any dividend may be paid to common stockholders, this balance must be entirely distributed to preferred shareholders. Conversely, in a non-cumulative issue, if a dividend payment is skipped, the preferred shareholder will never receive it.

Preference shares and bonds are practical ways for a company to raise money without issuing new common shares, which are more expensive and dilute voting rights. Banks, insurance companies and utilities are typical issuers of preferred stocks. The market for preferred shares is a small one, because only a fraction of listed companies issues preference shares.

From and investors’ perspective, since preferred securities include features of both bonds and stocks, they may help diversify and strengthen a fixed-income portfolio construction. Preferreds generally show indeed relatively low correlation to other fixed income sectors and equities, which means investing in them can improve overall portfolio diversification.

In the current environment of low interest rates and rising volatility, preference shares have a certain attraction. They have typically less sensitivity to risking interest rates. In certain tax jurisdictions, preferred shares can have a significant tax advantages, particularly where dividends are taxed lower than interest.

The exhibit below is designed to give the reader an idea of several relatively well-known issuers of preferred shares, and the types of yields available.

Exhibit 2: Selected preferreds based on dividend yield2

| Stock Symbol | Company name | Dividend Yield | Current Price | Annual Dividend | 52-Week High | 52-Week Low |

| AHT-D | Ashford Hospitality Trust Inc 8.45% Cum Pfd Ser D | 8.37% | $25.25 | $2.11 | 26.0 | 25.06 |

| C-N | Citigroup Capital XIII Tr Pfd Secs Fixed/Fltg | 8.33% | $27.18 | $2.26 | 27.81 | 25.85 |

| NYMTN | New York Mortgage Trust, Inc. 8% Cumulative Redeemable Perpetual Preferred Stock Series D | 8.29% | $24.12 | $2.00 | – | – |

| DX-B | Deutsche Bk Contingent Cap TR II Tr Pfd Sec | 7.89% | $24.17 | $1.91 | 25.16 | 23.25 |

| IVR-C | Invesco Mortgage Capital Inc Cumulative Redeemable Preferred Shares Series C | 7.36% | $25.46 | $1.88 | – | – |

| SHO-E | Sunstone Hotel Investors, Inc. 6.950% Series E Cumulative Redeemable Preferred Stock | 6.58% | $26.42 | $1.74 | 27.22 | 24.65 |

| BAC-W | Bank of America Corporation Deposit Shs Repr 1/1000th % Non-cumulative Preferred Shares Series W | 6.41% | $25.85 | $1.66 | – | – |

| Stock Symbol | Name | Avg. Volume | Net Assets | Yield | 2017 Return | 2018 YTD Return | Expense Ratio (net) |

| IPFF | iShares International Preferred Stock | 24,137 | $65.80 M | 3.68% | 22.88% | -3.09% | 0.55% |

| PSK | SPDR Wells Fargo Preferred Stock ETF | 104,466 | $669.11 M | 6.18% | 10.51% | 2.16% | 0.45% |

| PGX | Invesco Preferred ETF | 1,616,091 | $5.38 B | 5.65% | 10.47% | 2.15% | 0.50% |

| PGF | Invesco Financial Preferred ETF | 240,216 | $1.57 B | 5.41% | 10.81% | 1.55% | 0.63% |

This article is for informational purposes only, not to be construed as investment advice. Mention of specific equities if not an endorsement, merely to illustrate certain principles. It is very important to do your own investigation and analysis before making any investments based on your own personal circumstances.

1Data sources: Bloomberg, US Treasury Department.

2Divend.com: https://www.dividend.com/dividend-stocks/preferred-dividend-stocks.php#stocks&sort_name=dividend_yield&sort_order=desc&page=4

3 Investopedia.com. Information as of September 24, 2018.

2Divend.com: https://www.dividend.com/dividend-stocks/preferred-dividend-stocks.php#stocks&sort_name=dividend_yield&sort_order=desc&page=4

3 Investopedia.com. Information as of September 24, 2018.