While there are short-term fluctuations in interest rates caused by economic circumstances and central bank policies, there are also long-term structural trends affecting interest rates. This article will look in greater detail and one of the most important of these, namely demographics.

The thesis underpinning this article is that global demographics are likely to make the cost of capital more expensive over the coming decades, negatively affecting equity and asset prices. Allow me to walk you through the analysis.

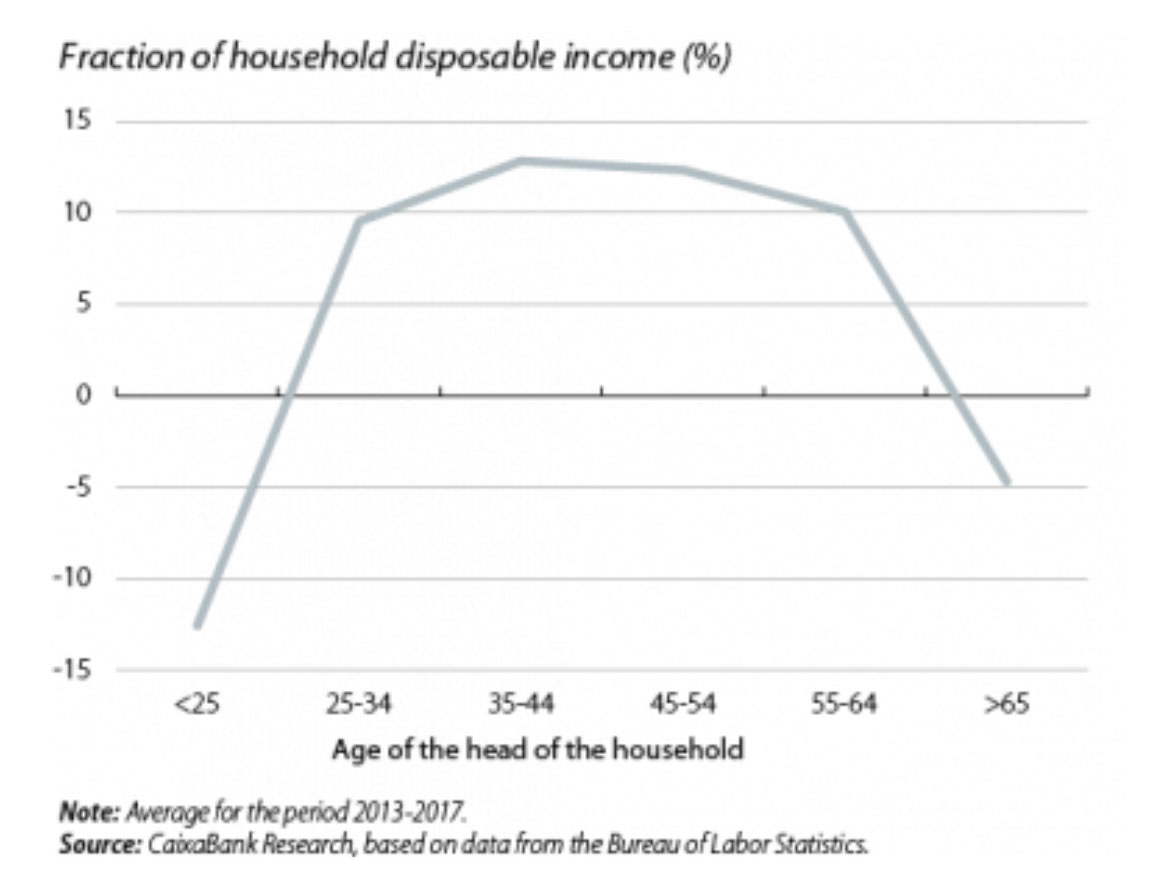

Fundamental to understanding the relationship between demographics and aging is the life cycle theory developed by Nobel laureates Franco Modigliani and Milton Friedman. Those in their 20’s and 30’s borrow to buy and furnish a home, bring children into the world, etc. Starting from their forties until retirement, they save, to pay off earlier borrowings and to fund retirement. Upon retirement, they abruptly switch from saving and begin liquidating assets to fund retirement. The life cycle curve looks like this:

The shape of this curve can be explained by the desire to maintain a stable quality of life over time.

So, the two main demographic trends hitting us today are (a) couples giving birth to fewer children; and (b) a demographic cliff, where the baby boomer generation suddenly goes into retirement. The baby boomers are the demographic equivalent of a pig working its way through a python. Post-World War II, new family formation and births reached an unprecedented peak. During the past few decades this age cohort became fantastically productive and saved huge amounts off money. Over the course of the next very few years, they are about to retire.

From a savings point of view, this is like throwing a switch. People who have been saving like crazy to squirrel away as many nuts as possible for their retirement—from one day to the next—begin using up those savings. Given the sheer numbers of people retiring in the next few years, this is likely to create big waves in savings and hence the supply of capital.

This trend is a global trend. It is even stronger in China, for example, than in the United States—first because there are more people going into retirement, both in absolute terms and relative to population size, but also because the Chinese have been much bigger savers than Americans or Europeans, because of the One Child Policy and lack of social security safety net in China. Economists have talked of a “savings glut” in China, which may very quickly swing to the opposite extreme.

A number of economists (e.g. Carvalho et al) believe that this demographic tailwind over the past few decades has contributed to a roughly 1.5-2% lower interest rate than otherwise would have prevailed. This demographic tailwind may soon disappear; indeed, the pendulum may swing the other way.

If you accept that the tailwind shifts to a headwind, and we are facing higher interest rates and cost of capital over the coming decades, how does this affect share and asset prices? The pricing of any asset is based on the risk-free cost of capital and the risk premium associated with the asset in question. Because of reduced savings (e.g. reduced supply of capital), risk-free cost of capital increases. And because much of those savings are still held by retirees, a higher risk premium may be required to fund riskier investments. So the pricing of all assets is likely to be affected, but riskier assets more so.

Of course, the trends discussed above will be favorable for savers. Bonds are likely to carry higher yields. In fact, baby boomers become more risk averse as they approach and pass retirement, they are likely to shift their portfolio from stocks into bonds. This will act as a headwind on equity valuations and potentially boost the value of bonds (partially offsetting higher yields caused by reduced availability of savings and capital).

What are trends that could dampen increasing cost of capital?

First, technological innovation tends to improve productivity and hence income and savings rates. Economies may be able to produce more with less labor, generating greater earnings and savings.

Second, should increasing life spans and health spans push back the retirement age, we might see a diminution of the effects talked about in this article. So far, due to Covid-19, the trend seems to have been towards early retirement. However, if Covid were to become a distant memory, this could theoretically change.

However, it is unlikely that either of these trends will outweigh the increased cost of capital. On balance, it is likelier that cost of capital will increase, creating a headwind of share and asset prices over the coming decades.

The thesis underpinning this article is that global demographics are likely to make the cost of capital more expensive over the coming decades, negatively affecting equity and asset prices. Allow me to walk you through the analysis.

Fundamental to understanding the relationship between demographics and aging is the life cycle theory developed by Nobel laureates Franco Modigliani and Milton Friedman. Those in their 20’s and 30’s borrow to buy and furnish a home, bring children into the world, etc. Starting from their forties until retirement, they save, to pay off earlier borrowings and to fund retirement. Upon retirement, they abruptly switch from saving and begin liquidating assets to fund retirement. The life cycle curve looks like this:

The shape of this curve can be explained by the desire to maintain a stable quality of life over time.

So, the two main demographic trends hitting us today are (a) couples giving birth to fewer children; and (b) a demographic cliff, where the baby boomer generation suddenly goes into retirement. The baby boomers are the demographic equivalent of a pig working its way through a python. Post-World War II, new family formation and births reached an unprecedented peak. During the past few decades this age cohort became fantastically productive and saved huge amounts off money. Over the course of the next very few years, they are about to retire.

From a savings point of view, this is like throwing a switch. People who have been saving like crazy to squirrel away as many nuts as possible for their retirement—from one day to the next—begin using up those savings. Given the sheer numbers of people retiring in the next few years, this is likely to create big waves in savings and hence the supply of capital.

This trend is a global trend. It is even stronger in China, for example, than in the United States—first because there are more people going into retirement, both in absolute terms and relative to population size, but also because the Chinese have been much bigger savers than Americans or Europeans, because of the One Child Policy and lack of social security safety net in China. Economists have talked of a “savings glut” in China, which may very quickly swing to the opposite extreme.

A number of economists (e.g. Carvalho et al) believe that this demographic tailwind over the past few decades has contributed to a roughly 1.5-2% lower interest rate than otherwise would have prevailed. This demographic tailwind may soon disappear; indeed, the pendulum may swing the other way.

If you accept that the tailwind shifts to a headwind, and we are facing higher interest rates and cost of capital over the coming decades, how does this affect share and asset prices? The pricing of any asset is based on the risk-free cost of capital and the risk premium associated with the asset in question. Because of reduced savings (e.g. reduced supply of capital), risk-free cost of capital increases. And because much of those savings are still held by retirees, a higher risk premium may be required to fund riskier investments. So the pricing of all assets is likely to be affected, but riskier assets more so.

Of course, the trends discussed above will be favorable for savers. Bonds are likely to carry higher yields. In fact, baby boomers become more risk averse as they approach and pass retirement, they are likely to shift their portfolio from stocks into bonds. This will act as a headwind on equity valuations and potentially boost the value of bonds (partially offsetting higher yields caused by reduced availability of savings and capital).

What are trends that could dampen increasing cost of capital?

First, technological innovation tends to improve productivity and hence income and savings rates. Economies may be able to produce more with less labor, generating greater earnings and savings.

Second, should increasing life spans and health spans push back the retirement age, we might see a diminution of the effects talked about in this article. So far, due to Covid-19, the trend seems to have been towards early retirement. However, if Covid were to become a distant memory, this could theoretically change.

However, it is unlikely that either of these trends will outweigh the increased cost of capital. On balance, it is likelier that cost of capital will increase, creating a headwind of share and asset prices over the coming decades.