The last time I recommended gold as an investment was in April, 2020, at which time it traded below $1700. By August, it ran up to over $2060. Since then, gold has gone through what, in my opinion, was a temporary correction, and has been trading again in the low 1700’s. As of the date of this article, gold is again showing some momentum, recently closing at $1777. While there are never any guarantees on future performance, it appears that gold is once again well positioned for a breakout. The reasons supporting this thesis are set out below:

1. In an environment of virtually every asset inflating, gold has been left out.

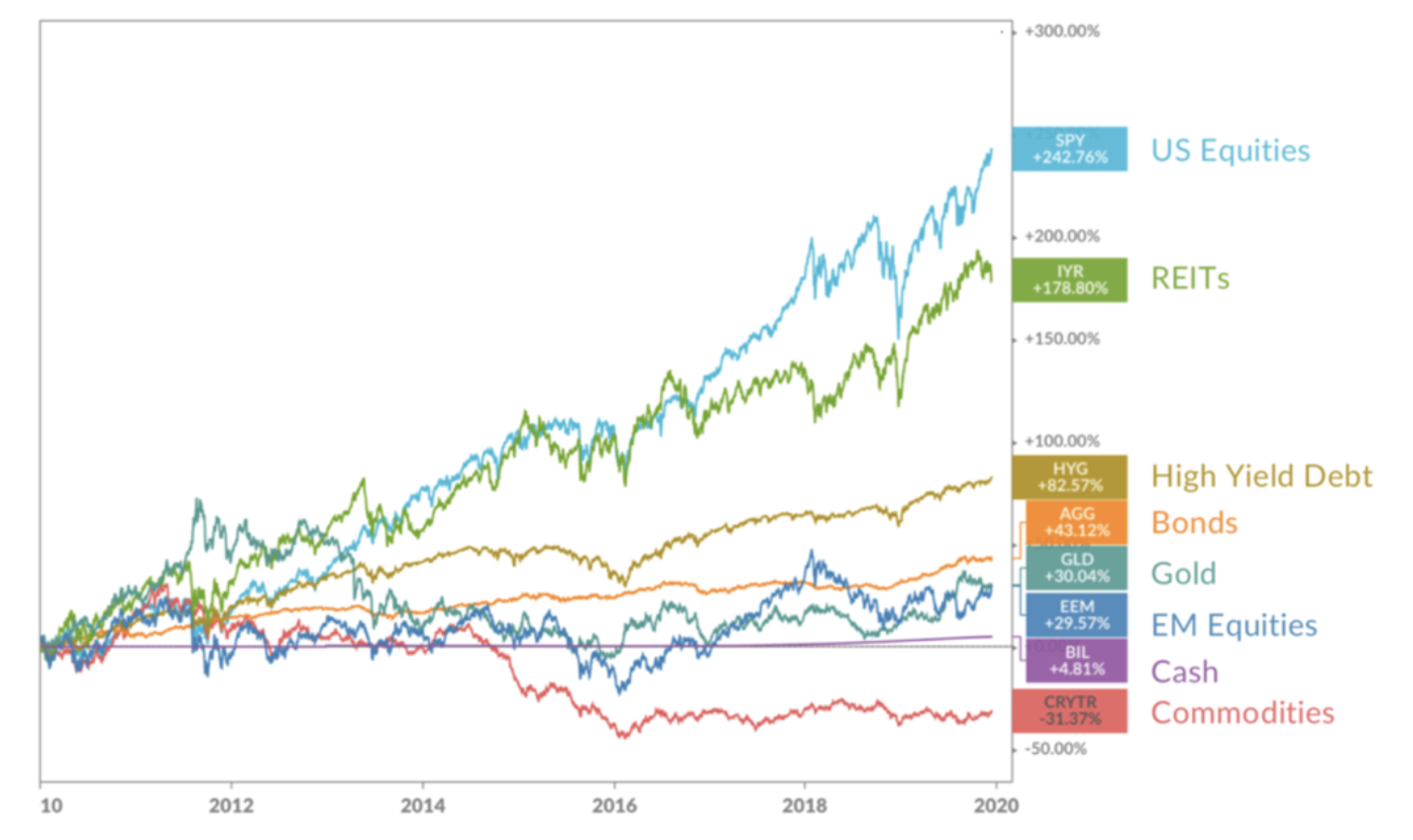

Over the past decade, gold has performed poorly as an asset class:

Exhibit 1: Total Return of Various Asset Classes from 2011 to 20201

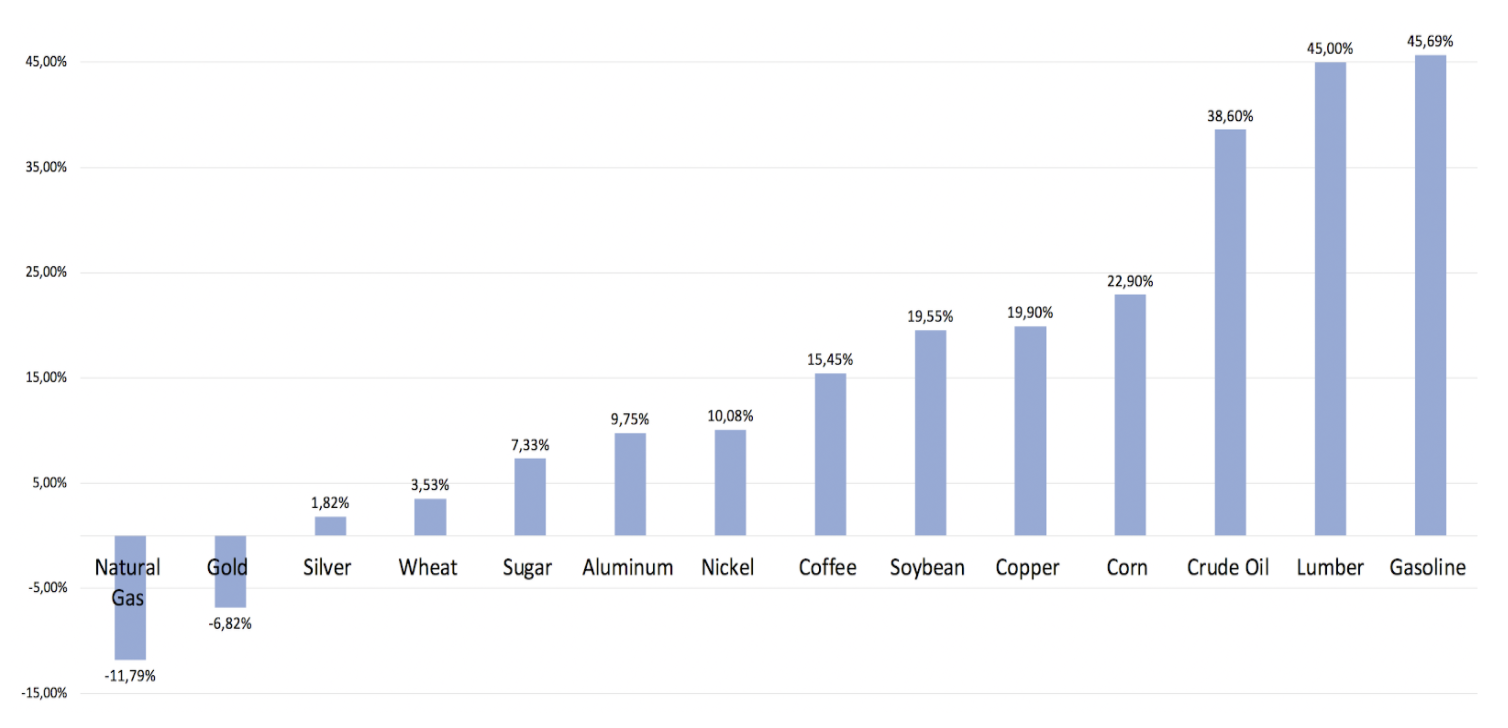

It has also recently been left behind by most commodities:

Exhibit 2: Average Return of different Commodities from November 2020 to April 16, 20212

In a market where high-flying tech stocks sell for 100-200x earnings and even more pedestrian publically listed companies are selling in the range of 30x earnings, it is refreshing to find gold mines for as low as 4-5x earnings.

2, When gold performs, it can perform spectacularly well

Gold moved from $243 in December 1970 to $1820 in January 1980, and from $401 in April 2001 to $2044 in November 20113 — five or sixfold moves over the course of a decade. Are we set for another golden decade?

3, There are strong macro tailwinds supporting gold

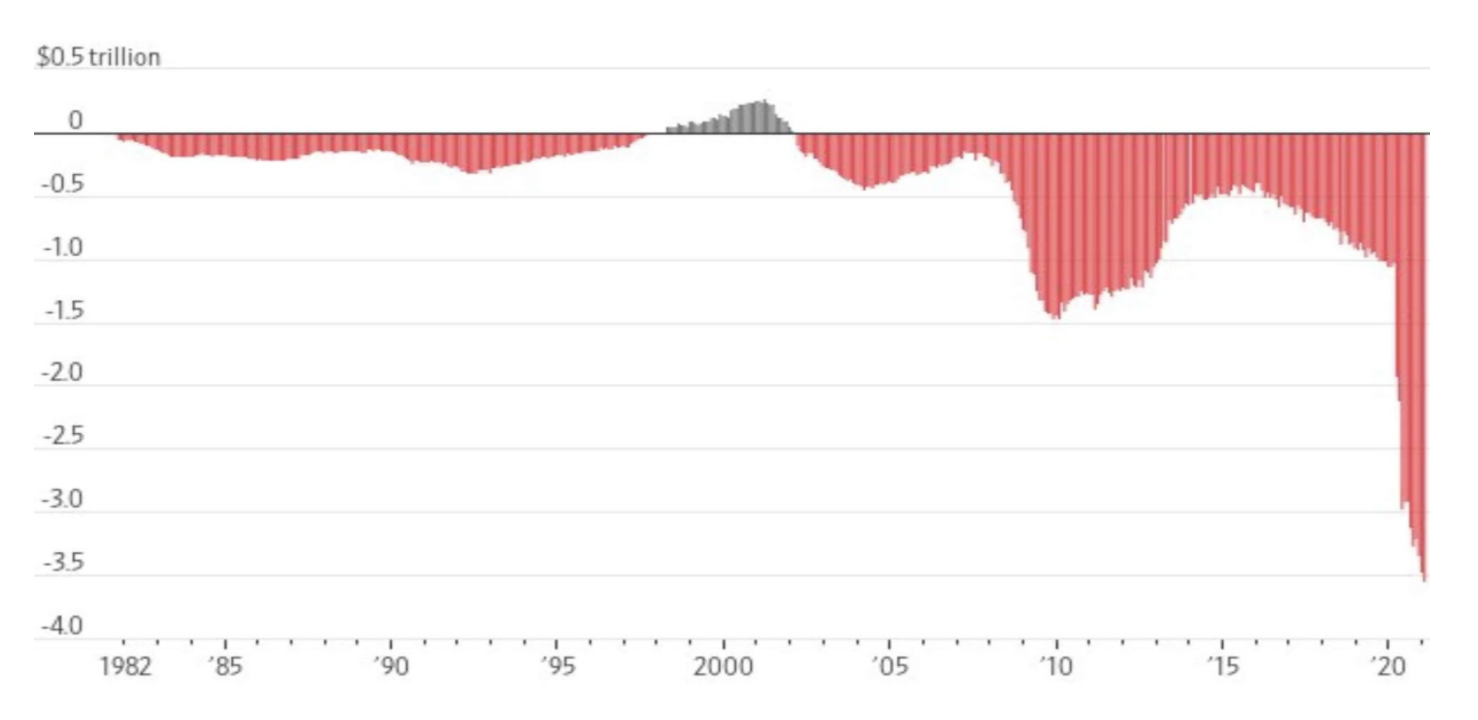

The majority of developed countries are engaged in both printing money and deficit spending on an unprecedented scale. In a past article, I explained how this is likely to result in inflation 4

Exhibit 3: US Federal Budget Deficits and Surpluses, 12-month Rolling Sum5

The magnitude of deficits today far surpass those of the 2008-9 recession. Fiscal stimulus direct to consumers distinguishes the current situation from 2008-9, increasing the chances of prolonged inflation.

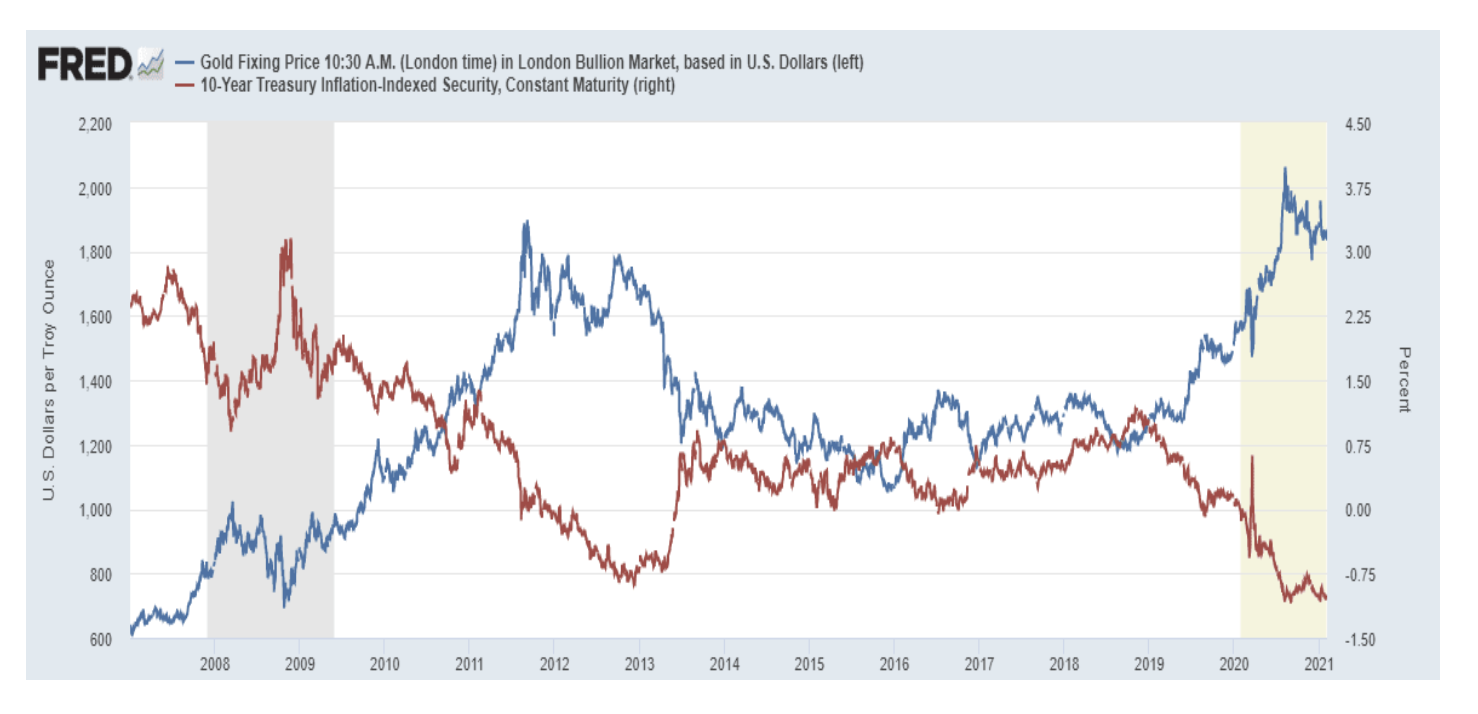

The price of gold correlates inversely with real interest rates:

Exhibit 4: Price of Gold inversely related to Interest Rates6

Global debt exceeds 350% of GDP. Rising interest rates are likely to trigger yield curve control (e.g. Governments buy bonds across various maturities to keep interest rates low across a broad spectrum of the yield curve). This will help Governments, individuals and corporations manage the interest costs of unprecedented debt levels. Yield curve control would result in very negative real interest rates – providing huge impetus for gold to rise.

Global debt exceeds 350% of GDP. Rising interest rates are likely to trigger yield curve control (e.g. Governments buy bonds across various maturities to keep interest rates low across a broad spectrum of the yield curve). This will help Governments, individuals and corporations manage the interest costs of unprecedented debt levels. Yield curve control would result in very negative real interest rates – providing huge impetus for gold to rise.

4, Digital Currencies will create an Opportunity for Gold

Many claim that bitcoin diminishes appetite for gold. I see a different trend: as cash is displaced by digital currencies and bitcoin, gold will be the only way to stay “off grid” and maintain privacy and anonymity. This desire will increase if Governments use digital currency as policy instruments (e.g. putting expiry dates on digital currency, or making it spendable only on certain types of goods)7.

5, Gold as a Hedge

Gold has a low correlation to equities and most other asset classes. The World Gold Council suggests that keeping 4-5% of an investment portfolio in gold creates an excellent hedge8, (e.g. portfolio return is augmented for a given degree of risk).

6, Insurance against the “Great Reset”

A number of economists are predicting a “crack up boom”, where money printing and deficits lead to a rapid inflation, complete loss of confidence in fiat currencies and eventual currency collapse.

If major Central Banks, the largest holders of gold, would revalue and make a market for gold at say $50,000/oz, most countries would have sufficient gold reserves to collateralize national debt. This would be the simplest and most elegant solution to the world’s debt crisis.

In conclusion, gold is the ultimate monetary insurance. There are some valid reasons for holding up to 5% of your portfolio in gold.Since global gold holdings are a small fraction of bond and equity holdings, even a small shift towards gold could have a large impact on price.

Caveat: this article is not to be construed as investment advice. Readers are advised to perform their own due diligence. The author owns positions in physical gold, ETF’s and gold-related equities.

1. In an environment of virtually every asset inflating, gold has been left out.

Over the past decade, gold has performed poorly as an asset class:

Exhibit 1: Total Return of Various Asset Classes from 2011 to 20201

It has also recently been left behind by most commodities:

Exhibit 2: Average Return of different Commodities from November 2020 to April 16, 20212

In a market where high-flying tech stocks sell for 100-200x earnings and even more pedestrian publically listed companies are selling in the range of 30x earnings, it is refreshing to find gold mines for as low as 4-5x earnings.

2, When gold performs, it can perform spectacularly well

Gold moved from $243 in December 1970 to $1820 in January 1980, and from $401 in April 2001 to $2044 in November 20113 — five or sixfold moves over the course of a decade. Are we set for another golden decade?

3, There are strong macro tailwinds supporting gold

The majority of developed countries are engaged in both printing money and deficit spending on an unprecedented scale. In a past article, I explained how this is likely to result in inflation 4

Exhibit 3: US Federal Budget Deficits and Surpluses, 12-month Rolling Sum5

The magnitude of deficits today far surpass those of the 2008-9 recession. Fiscal stimulus direct to consumers distinguishes the current situation from 2008-9, increasing the chances of prolonged inflation.

The price of gold correlates inversely with real interest rates:

Exhibit 4: Price of Gold inversely related to Interest Rates6

Global debt exceeds 350% of GDP. Rising interest rates are likely to trigger yield curve control (e.g. Governments buy bonds across various maturities to keep interest rates low across a broad spectrum of the yield curve). This will help Governments, individuals and corporations manage the interest costs of unprecedented debt levels. Yield curve control would result in very negative real interest rates – providing huge impetus for gold to rise.4, Digital Currencies will create an Opportunity for Gold

Many claim that bitcoin diminishes appetite for gold. I see a different trend: as cash is displaced by digital currencies and bitcoin, gold will be the only way to stay “off grid” and maintain privacy and anonymity. This desire will increase if Governments use digital currency as policy instruments (e.g. putting expiry dates on digital currency, or making it spendable only on certain types of goods)7.

5, Gold as a Hedge

Gold has a low correlation to equities and most other asset classes. The World Gold Council suggests that keeping 4-5% of an investment portfolio in gold creates an excellent hedge8, (e.g. portfolio return is augmented for a given degree of risk).

6, Insurance against the “Great Reset”

A number of economists are predicting a “crack up boom”, where money printing and deficits lead to a rapid inflation, complete loss of confidence in fiat currencies and eventual currency collapse.

“In any monetary reset, countries will come together and sit around the table. One can think of that meeting as a poker game. When you sit down at the poker table, you want a big pile of chips. Gold functions like a pile of poker chips in this context. This doesn’t mean that the world automatically goes to a gold standard. It does mean that your voice at the table is going to be a function of the size of your gold hoard.” (James Rickards)8

If major Central Banks, the largest holders of gold, would revalue and make a market for gold at say $50,000/oz, most countries would have sufficient gold reserves to collateralize national debt. This would be the simplest and most elegant solution to the world’s debt crisis.

In conclusion, gold is the ultimate monetary insurance. There are some valid reasons for holding up to 5% of your portfolio in gold.Since global gold holdings are a small fraction of bond and equity holdings, even a small shift towards gold could have a large impact on price.

Caveat: this article is not to be construed as investment advice. Readers are advised to perform their own due diligence. The author owns positions in physical gold, ETF’s and gold-related equities.

1Koyfin

2Capital IQ

3https://www.macrotrends.net/1333/historical-gold-prices-100-year-chart

4https://europhoenix.com/blog/inflation-or-deflation-by-les-nemethy-former-world-banker-ceo-euro-phoenix-financial-advisors-ltd/

5U.S Treasury

6Board of Governors; St Louis Fed; IBA

7https://www.youtube.com/watch?v=gYr4_3Tcuqg

8https://www.gold.org/goldhub/research/gold-and-tail-risk-hedging-international-perspective

9The New Case for Gold, James Rickards, 2016

2Capital IQ

3https://www.macrotrends.net/1333/historical-gold-prices-100-year-chart

4https://europhoenix.com/blog/inflation-or-deflation-by-les-nemethy-former-world-banker-ceo-euro-phoenix-financial-advisors-ltd/

5U.S Treasury

6Board of Governors; St Louis Fed; IBA

7https://www.youtube.com/watch?v=gYr4_3Tcuqg

8https://www.gold.org/goldhub/research/gold-and-tail-risk-hedging-international-perspective

9The New Case for Gold, James Rickards, 2016