Our last article was on control premiums. Minority discount is basically the flipside of control premium

: in the same way that a premium applies when you purchase 51% of shares that make 100% of the decisions, so too a discount applies when you purchase 49% of shares that make few or no decisions as related to the corporate governance of a company.

The fewer the rights associated with the minority stake, the higher the discount. We will examine some of the factors that might affect the extent of the discount:

Firstly, statutes, articles of incorporation, shareholders’ agreements or bylaws may require a supermajority to approve certain actions. For instance, in some jurisdictions an approval of specific corporate actions as sale of assets or liquidation of the company may require a two-thirds majority instead of a simple majority. As a result, a shareholder with a one-third ownership interest in the company may block such actions (and hence have more value than without blocking rights, the discount depending on extent of blocking rights).

Secondly, the distribution of equity ownership has an important bearing on relative rights of shareholders. For example, if a company is owned by three shareholders holding equity interest (33.33% each), no one has absolute control, and no one is in a relatively inferior position to the other two. (Neither of the three shareholders may have a control premium in such a case; if there is a pattern of two shareholders voting together, the shares of the third shareholder may nevertheless have a discount).

Thirdly, variation in minority discounts may result from “differences in the extent to which the minority stockholders are economically disadvantaged”1. Basically, a company is well run, and all shareholders receive the same pro rata returns to capital, then the minority discount will be less.

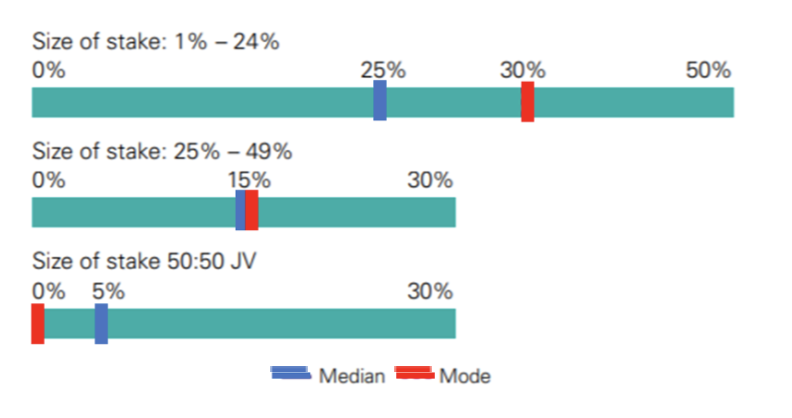

Trustworthy statistics on the size of minority discounts are scarce. While every situation is specific, and depends on the individual facts of the situation, the following chart may provide some very general “rule of thumb” guidance:

Exhibit 1: What discount do you apply in valuing a minority interest?2 *The mode is a statistical term that refers to the most frequently occurring number found in a set of numbers

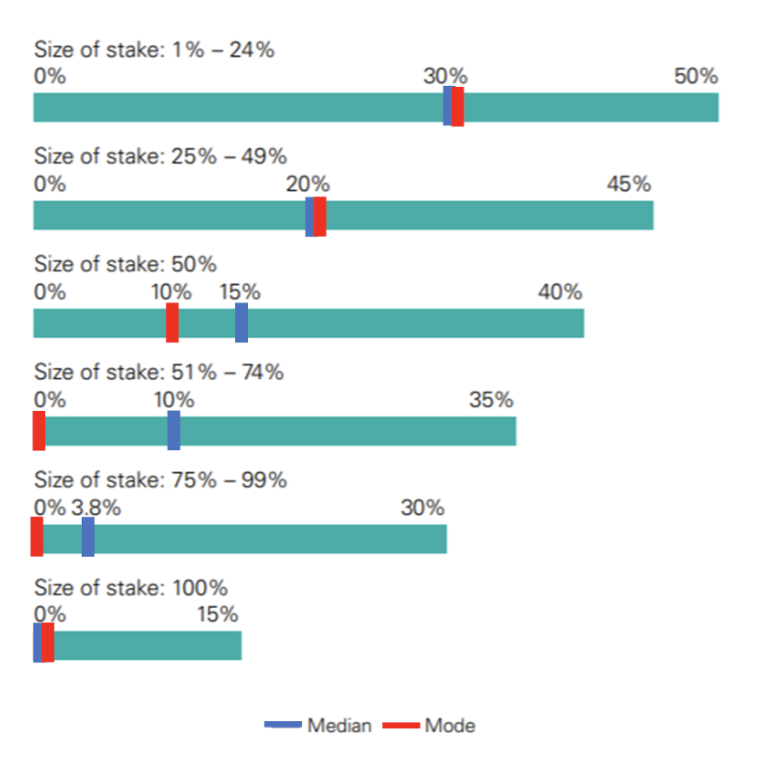

The concept of minority discount is consistent with the concepts of marketability and lack of marketability. However, it is important to distinguish between a discount for lack of ownership control (minority discount) and a discount for lack of marketability. The concept of marketability deals with liquidity of the subject ownership interest – that is, how quickly and certainly it can be converted to cash at the owner’s discretion3. A discount for a lack of marketability may be even applied to a 100% ownership interest in a closely held enterprise, as it may take months and requires significant expenses and efforts to prepare and sell a 100% ownership interest.

Exhibit 2: When a marketability discount is required, what sized discount do you apply?4

*The mode is a statistical term that refers to the most frequently occurring number found in a set of numbers

The concept of minority discount is consistent with the concepts of marketability and lack of marketability. However, it is important to distinguish between a discount for lack of ownership control (minority discount) and a discount for lack of marketability. The concept of marketability deals with liquidity of the subject ownership interest – that is, how quickly and certainly it can be converted to cash at the owner’s discretion3. A discount for a lack of marketability may be even applied to a 100% ownership interest in a closely held enterprise, as it may take months and requires significant expenses and efforts to prepare and sell a 100% ownership interest.

Exhibit 2: When a marketability discount is required, what sized discount do you apply?4

The following exhibit illustrates the relationship between controlling and non-controlling ownership interest value, and marketability and lack of marketability.

Exhibit 3: Example of Relationships between Levels of Ownership Interest and Applicability of Valuation Discounts5

The following exhibit illustrates the relationship between controlling and non-controlling ownership interest value, and marketability and lack of marketability.

Exhibit 3: Example of Relationships between Levels of Ownership Interest and Applicability of Valuation Discounts5

* The magnitude of the valuation discounts is selected for illustrative purposes only and not to indicate recommended levels (or even orders of magnitude) of specific valuation adjustments.

** The cumulative impact of a 10%, a 30% and a 40% discount is a total 62.2% (and not an 80% discount). This is because the application of valuation discounts is multiplicative and not additive. Also, the order of the application of the valuation discounts will not affect the cumulative amount of the valuation adjustment.

The types and amounts of appropriate discounts often cause significant disputes and controversies during valuations. It would be an error to apply the above discounts too rigidly—every situation requires careful analysis of facts and considerable judgment.

The fewer the rights associated with the minority stake, the higher the discount. We will examine some of the factors that might affect the extent of the discount:

Firstly, statutes, articles of incorporation, shareholders’ agreements or bylaws may require a supermajority to approve certain actions. For instance, in some jurisdictions an approval of specific corporate actions as sale of assets or liquidation of the company may require a two-thirds majority instead of a simple majority. As a result, a shareholder with a one-third ownership interest in the company may block such actions (and hence have more value than without blocking rights, the discount depending on extent of blocking rights).

Secondly, the distribution of equity ownership has an important bearing on relative rights of shareholders. For example, if a company is owned by three shareholders holding equity interest (33.33% each), no one has absolute control, and no one is in a relatively inferior position to the other two. (Neither of the three shareholders may have a control premium in such a case; if there is a pattern of two shareholders voting together, the shares of the third shareholder may nevertheless have a discount).

Thirdly, variation in minority discounts may result from “differences in the extent to which the minority stockholders are economically disadvantaged”1. Basically, a company is well run, and all shareholders receive the same pro rata returns to capital, then the minority discount will be less.

Trustworthy statistics on the size of minority discounts are scarce. While every situation is specific, and depends on the individual facts of the situation, the following chart may provide some very general “rule of thumb” guidance:

Exhibit 1: What discount do you apply in valuing a minority interest?2

*The mode is a statistical term that refers to the most frequently occurring number found in a set of numbers

The concept of minority discount is consistent with the concepts of marketability and lack of marketability. However, it is important to distinguish between a discount for lack of ownership control (minority discount) and a discount for lack of marketability. The concept of marketability deals with liquidity of the subject ownership interest – that is, how quickly and certainly it can be converted to cash at the owner’s discretion3. A discount for a lack of marketability may be even applied to a 100% ownership interest in a closely held enterprise, as it may take months and requires significant expenses and efforts to prepare and sell a 100% ownership interest.

Exhibit 2: When a marketability discount is required, what sized discount do you apply?4

The following exhibit illustrates the relationship between controlling and non-controlling ownership interest value, and marketability and lack of marketability.

Exhibit 3: Example of Relationships between Levels of Ownership Interest and Applicability of Valuation Discounts5

| Level of Ownership Interest | Example of Ownership Interest Type | Type of Applicable Valuation Adjustment | Illustrative Impact of Value Decrement | Illustrative Percentage Discount* |

| Marketable, controlling ownership interest | 100% ownership of a business that is offered for sale | No discount applicable | $10.00 per share | N/A |

| Non-marketable, controlling ownership interest | Less than 100% (but controlling) owners | Discount for illiquidity at the business enterprise level | $9.00 per share | 10% |

| Marketable, non-controlling ownership interest | Shares of registered stock in a publicly traded corporation | Discount for lack of control (also called a minority interest discount) | $6.30 per share | 30% |

| Non-marketable, non-controlling ownership interest | Shares of stock in a closely held o family owned business | Discount for lack of marketability at the share level | $3.78 per share* | 40% |

The types and amounts of appropriate discounts often cause significant disputes and controversies during valuations. It would be an error to apply the above discounts too rigidly—every situation requires careful analysis of facts and considerable judgment.

1Control Premiums, Minority Discounts, and Marketability Discounts by Philip Saunders, Jr., Ph.D.

2For all it’s worth. KPMG Valuation Practices Survey 2017

3Value a Business by Shannon Pratt, Robert Reilly and Robert Schweihs

4For all it’s worth. KPMG Valuation Practices Survey 2017

5Value a Business by Shannon Pratt, Robert Reilly and Robert Schweihs

2For all it’s worth. KPMG Valuation Practices Survey 2017

3Value a Business by Shannon Pratt, Robert Reilly and Robert Schweihs

4For all it’s worth. KPMG Valuation Practices Survey 2017

5Value a Business by Shannon Pratt, Robert Reilly and Robert Schweihs