Our firm recently performed two valuations on a pharmaceutical company two years apart.

The owners were surprised by the surprisingly large jump in value, far larger than performance improvement might have justified. We of course reported back to him in some detail, and the answer lay in the change in capital structure, namely the company had layered on a significant amount of very cheap debt (interest rate in the range of 2%). In a Discounted Cash Flow valuation, this affects Weighted Average Cost of Capital (WACC), the discount rate applied to valuation of future cash flows.

Optimizing capital structure involves achieving and maintaining an optimal debt / equity ratio that maximizes a company’s market value, while minimizing cost of capital. Capital structure must also take into account the need to create an adequate liquidity cushion, to face a possible downturn and scarcity of funding. A company needs to choose between a variety of financing instruments, addressing multiple needs, including credit impact, accounting impact, and shareholder dilution.

The cost of capital is based on a company’s capital structure (debt vs equity, or hybrid instruments) and the cost of each component. A company may minimize its cost of capital by lowering the cost of debt or equity or via capital restructuring, namely changing debt and equity as it appears on the balance sheet:

Exhibit 1: A stylized balance sheet of a non-financial firm 1 In the above stylized balance sheet, on the right side we see sources of funds (various types of debt, equity, hybrid instruments, etc.)2. Equity may come from capital injections, retained earnings after payment of dividends, etc. On the left hand side, we see the uses of those funds. Optimizing cost of capital involves restructuring the right hand side of the balance sheet, namely source of funds.

In the above stylized balance sheet, on the right side we see sources of funds (various types of debt, equity, hybrid instruments, etc.)2. Equity may come from capital injections, retained earnings after payment of dividends, etc. On the left hand side, we see the uses of those funds. Optimizing cost of capital involves restructuring the right hand side of the balance sheet, namely source of funds.

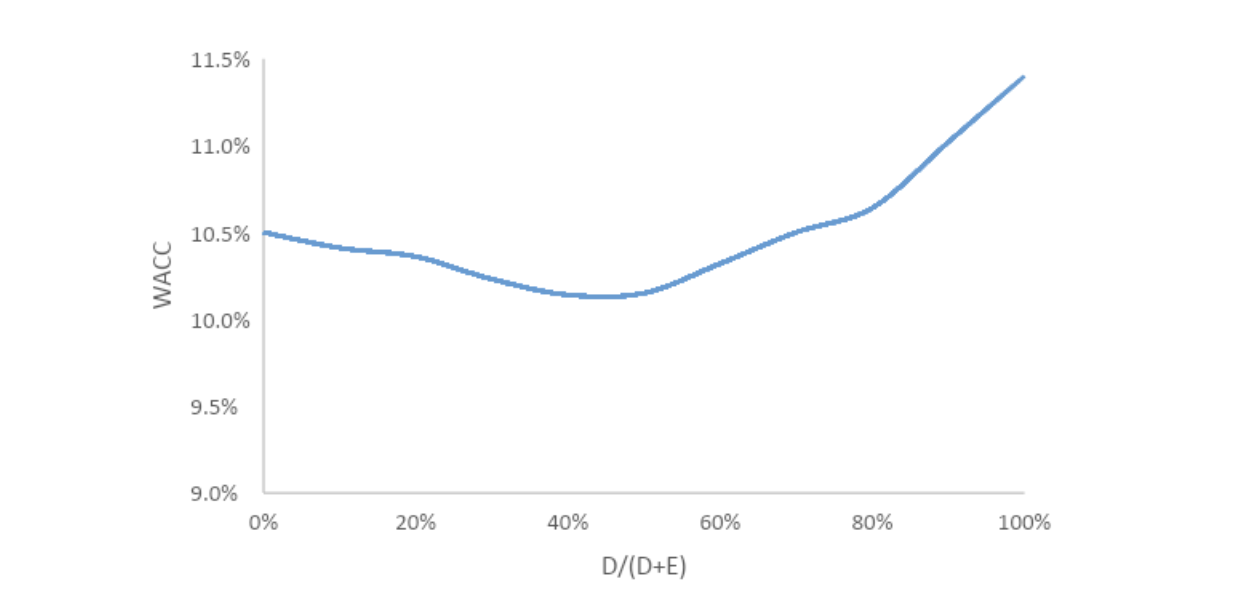

Theoretically, debt offers the lowest cost of capital due to lower risk levels than equity, and in most jurisdictions, tax deductibility. To a certain point increasing a company’s debt ratio reduces its cost of capital. However, too much debt increases financial risk, hence increasing the return on equity required by shareholders. Thus, in theory a company needs to find the optimal point at which the marginal benefit of debt equals the marginal cost, which is illustrated in Exhibit 2, where the cost of capital happens to reach its lowest value at a debt/total capital ratio of 40%.

Exhibit 2: Hypothetical Debt Ratios and Weighted Average Cost of Capital (WACC) 3

Besides optimizing capital structure, a company may also reduce its cost of capital by lowering costs of debt and equity. On the debt side, this may involve creating competition among banks to reduce debt costs, replacing bank debt with debentures, etc. On the equity side, it might involve creating a class of preferred shares or other hybrid instrument.

Besides optimizing capital structure, a company may also reduce its cost of capital by lowering costs of debt and equity. On the debt side, this may involve creating competition among banks to reduce debt costs, replacing bank debt with debentures, etc. On the equity side, it might involve creating a class of preferred shares or other hybrid instrument.

Cost of debt is the market interest rate that the firm has to pay on its borrowing. It will depend upon three components: 4:

In our experience, most owners of mid-sized companies do not give sufficient consideration to issues of capital structure prior to raising capital or putting a company up for sale. This may, in fact, result in leaving quite a bit of money on the table. When private equity owners invest in a company, this type of “financial engineering” is part of their value added. However, there is no reason why company owners should not give attention to this matter prior to bringing on board any investor. Indeed, it should be periodically reviewed independent of any transaction. Why pay more than necessary for capital?

Optimizing capital structure involves achieving and maintaining an optimal debt / equity ratio that maximizes a company’s market value, while minimizing cost of capital. Capital structure must also take into account the need to create an adequate liquidity cushion, to face a possible downturn and scarcity of funding. A company needs to choose between a variety of financing instruments, addressing multiple needs, including credit impact, accounting impact, and shareholder dilution.

The cost of capital is based on a company’s capital structure (debt vs equity, or hybrid instruments) and the cost of each component. A company may minimize its cost of capital by lowering the cost of debt or equity or via capital restructuring, namely changing debt and equity as it appears on the balance sheet:

Exhibit 1: A stylized balance sheet of a non-financial firm 1

In the above stylized balance sheet, on the right side we see sources of funds (various types of debt, equity, hybrid instruments, etc.)2. Equity may come from capital injections, retained earnings after payment of dividends, etc. On the left hand side, we see the uses of those funds. Optimizing cost of capital involves restructuring the right hand side of the balance sheet, namely source of funds.

Theoretically, debt offers the lowest cost of capital due to lower risk levels than equity, and in most jurisdictions, tax deductibility. To a certain point increasing a company’s debt ratio reduces its cost of capital. However, too much debt increases financial risk, hence increasing the return on equity required by shareholders. Thus, in theory a company needs to find the optimal point at which the marginal benefit of debt equals the marginal cost, which is illustrated in Exhibit 2, where the cost of capital happens to reach its lowest value at a debt/total capital ratio of 40%.

Exhibit 2: Hypothetical Debt Ratios and Weighted Average Cost of Capital (WACC) 3

| Debt Ratio D/(D+E) | Cost of Equity ke | Cost of Debt kd | After-tax Cost of Debt (Tax rate = 40%) | WACC |

| 0 | 10.5% | 8.0% | 4.8% | 10.50% |

| 10% | 11.0% | 8.5% | 5.1% | 10.41% |

| 20% | 11.6% | 9.0% | 5.4% | 10.36% |

| 30% | 12.3% | 9.0% | 5.4% | 10.23% |

| 40% | 13.1% | 9.5% | 5.7% | 10.14% |

| 50% | 14.0% | 10.5% | 6.3% | 10.15% |

| 60% | 15.0% | 12.0% | 7.2% | 10.32% |

| 70% | 16.1% | 13.5% | 8.1% | 10.50% |

| 80% | 17.2% | 15.0% | 9.0% | 10.64% |

| 90% | 18.4% | 17.0% | 10.2% | 11.02% |

| 100% | 19.7% | 19.0% | 11.4% | 11.40% |

Besides optimizing capital structure, a company may also reduce its cost of capital by lowering costs of debt and equity. On the debt side, this may involve creating competition among banks to reduce debt costs, replacing bank debt with debentures, etc. On the equity side, it might involve creating a class of preferred shares or other hybrid instrument.

Cost of debt is the market interest rate that the firm has to pay on its borrowing. It will depend upon three components: 4:

- a, The general level of interest rates

- b, The default premium

- c, A firm’s tax rate

In our experience, most owners of mid-sized companies do not give sufficient consideration to issues of capital structure prior to raising capital or putting a company up for sale. This may, in fact, result in leaving quite a bit of money on the table. When private equity owners invest in a company, this type of “financial engineering” is part of their value added. However, there is no reason why company owners should not give attention to this matter prior to bringing on board any investor. Indeed, it should be periodically reviewed independent of any transaction. Why pay more than necessary for capital?

1Deleveraging, Investing and Optimizing Capital Structure by Stefano Gatti and Carlo Chiarella

2ibid

3Finding the Right Financing Mix: The Capital Structure Decision by Aswath Damodaran

4ibid

2ibid

3Finding the Right Financing Mix: The Capital Structure Decision by Aswath Damodaran

4ibid